Tax Thresholds 2025 – UK Income Tax Bands and NI Rates

The 2025/26 tax year begins on 6 April with unchanged income tax thresholds for most UK workers. The personal allowance remains frozen at £12,570, maintaining the freeze first announced in 2021 and extended to 2028. This static threshold continues to pull earners into higher tax brackets as wages rise with inflation, a phenomenon economists term fiscal drag.

The official rates and allowances published by HMRC confirm no adjustments to the main bands for England, Wales, and Northern Ireland. Scotland retains its devolved six-band system, while National Insurance contributions see threshold alignments but no major rate cuts following the reductions implemented in 2024.

Self-employed workers face similar freezes on Class 4 National Insurance thresholds, though the small profits threshold for Class 2 contributions remains at £6,725. Understanding these fixed thresholds proves essential for accurate budgeting and tax planning throughout the financial year.

What are the income tax thresholds for 2025/26?

The UK maintains a tiered income tax system where earnings above the personal allowance face progressively higher rates. For the 2025/26 tax year, the primary threshold stands at £12,570 for zero-rate taxation across all regions.

| Personal Allowance | Basic Rate Cap | Higher Rate Start | Additional Rate Start |

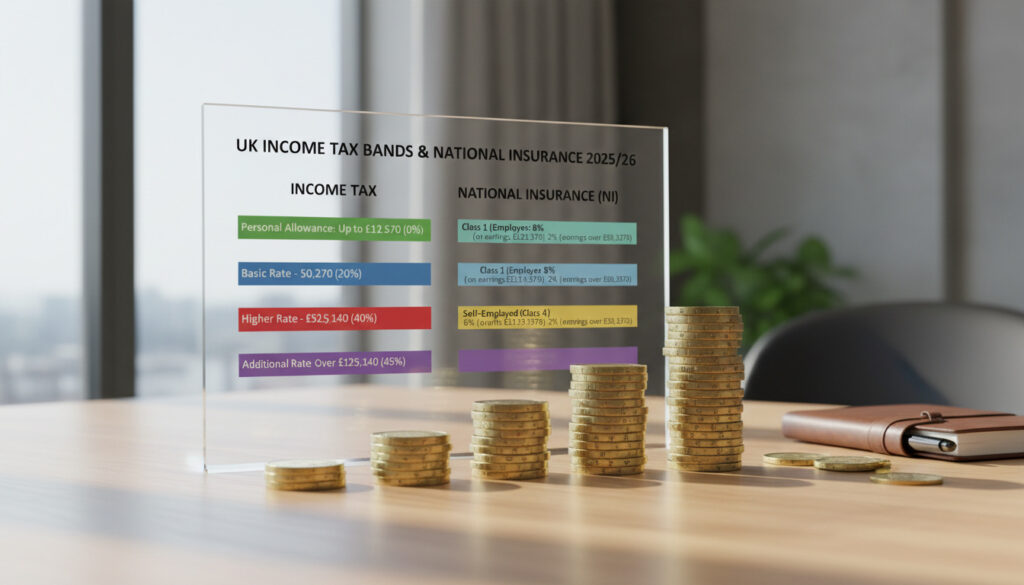

| £12,570 (frozen) | £50,270 | £50,271 | £125,140 |

- The personal allowance has remained static at £12,570 since 2021/22

- Basic rate taxpayers pay 20% on earnings between £12,571 and £50,270

- Higher rate (40%) kicks in immediately above £50,270

- Additional rate threshold dropped to £125,140 in 2023/24 and remains there

- Fiscal drag will push over two million additional earners into higher bands by 2028

- Scottish taxpayers face six distinct bands rather than three

- Employer National Insurance thresholds freeze at £5,000 annually

| Tax Band | Annual Earnings (England, Wales, NI) | Rate |

|---|---|---|

| Personal Allowance | Up to £12,570 | 0% |

| Basic Rate | £12,571 – £50,270 | 20% |

| Higher Rate | £50,271 – £125,140 | 40% |

| Additional Rate | Above £125,140 | 45% |

| Scotland Specific Bands | ||

| Starter Rate | £12,571 – £15,397 | 19% |

| Basic Rate | £15,398 – £27,491 | 20% |

| Intermediate Rate | £27,492 – £62,430 | 21% |

| Higher Rate | £62,431 – £125,140 | 42% |

| Advanced Rate | £62,431 – £125,140 (overlapping range noted in technical guidance) | 45% |

| Top Rate | Above £125,140 | 48% |

What are National Insurance thresholds for 2025?

National Insurance contributions fund state benefits and the NHS. For employees, Class 1 NICs apply to earnings above the primary threshold, while employers pay Class 1 secondary contributions above a separate limit. The 2025/26 rates reflect the alignment of employee thresholds with income tax personal allowances, a structure unchanged since 2024.

Employee Class 1 Contributions

Workers begin paying National Insurance at 15% on earnings above £242 weekly, £1,048 monthly, or £12,570 annually. The upper earnings limit remains fixed at £50,270 per year, matching the higher rate income tax threshold. Earnings above this limit continue to attract a reduced NICs rate, effectively 2% for the portion above the threshold.

Self-Employed Tax Obligations

Self-employed individuals navigate Class 2 and Class 4 contributions. Class 2 payments remain at £0 for those earning above the small profits threshold but below £6,725, effectively making this a zero-cost category. Class 4 charges 9% on profits between £12,571 and £50,270, dropping to 2% on amounts above, mirroring the employed upper earnings limit structure. The self-employed guide confirms these thresholds remain frozen to match the personal allowance.

Employers pay Class 1 National Insurance at 15% on wages exceeding £5,000 annually (£96 weekly, £417 monthly). This threshold represents a significant differential from the employee primary threshold, creating a band where employer contributions apply but employee contributions do not.

What are Scotland’s tax bands for 2025?

Scotland exercises devolved tax powers through the Scottish Parliament, maintaining a six-band structure that diverges significantly from the three-band system elsewhere. The detailed Scottish bands create a more graduated progression, with rates ranging from 19% to 48%.

The starter rate offers a 1% discount compared to England’s basic rate for the lowest earners, while intermediate and higher bands capture middle-income workers earlier than the rest of the UK. Scottish taxpayers earning between £27,492 and £62,430 face a 21% intermediate rate that has no direct equivalent south of the border.

Technical documentation reveals overlapping definitions for Scotland’s higher and advanced bands, with some sources indicating the advanced rate begins at £62,431 while higher rate calculations extend to £125,140. Taxpayers should verify specific calculations using Scottish Revenue software rather than standard UK calculators.

Cross-Border Comparisons

A Scottish earner on £45,000 pays tax at 19% on the first £2,827 above the allowance, 20% on the next £12,094, and 21% on the remaining £17,909. The same salary in England would attract a flat 20% on the £32,430 taxable amount. Higher earners above £125,140 face a 48% top rate in Scotland versus 45% elsewhere, creating the widest divergence at the upper income levels.

Have tax thresholds changed for 2025?

No substantive changes affect the main income tax thresholds for 2025/26. The personal allowance, basic rate limit, and higher rate threshold remain frozen at 2021/22 levels following the Chancellor’s 2022 Autumn Statement extension to 2027/28. This freeze represents the longest sustained period of fiscal drag in recent decades, deliberately increasing the tax burden as nominal wages rise with inflation.

The Office for Budget Responsibility analysis indicates this policy will create over two million additional higher-rate taxpayers by the freeze’s conclusion. The additional rate threshold reduction to £125,140, implemented in 2023/24 to coincide with the personal allowance taper point, remains unchanged.

When thresholds remain fixed while wages increase, taxpayers cross into higher bands despite no real income improvement. A worker earning £48,000 in 2021 who receives 3% annual pay rises will breach the £50,270 higher rate threshold by 2026, increasing their marginal tax rate from 20% to 40% on earnings above the limit.

When do 2025/26 tax thresholds take effect?

- : Personal allowance freeze begins, initially planned until 2025/26.

- : Autumn Statement extends the freeze to 2027/28.